Part I – Dissimilarity Index

White compared to Black:

∑ |a-b|

= 90.56

DI = 45.28 – meaning 45.28% of black people

would have to move in order to have an equal distribution of white people and

black people.

White

compared to Asian:

∑ |a-b|

= 78.93

DI = 39.46 – meaning 39.46% of Asians would

have to move in order to have an equal distribution of white people and Asians.

White

compared to Hispanic:

∑ |a-b|

= 77.45

DI = 38.73 – meaning 45.28% of Hispanics

would have to move in order to have an equal distribution of white people and

Hispanics.

|

| Map of Dune County with the percentage of minorities by census tract. |

These

results show that around 40% of the population would have to move in order to

have an even distribution of the races in each census tract. The maps show that

Non-Whites are by far concentrated in the central parts of Madison and Dane

County. Non-whites would have to move out into the suburbs of Madison and the

surround small towns in Dane County in order to have an equal distribution of

Whites and Non-whites.

Part II – Kitchen Sink

|

| SPSS results of a Kitchen Sink Approach. |

Hypotheses

The

Null Hypothesis is that there is no linear relationship between Number of

Foreclosures per 100 persons and High Cost Loans. The Alternative Hypothesis is

that there is a linear relationship between Number of Foreclosures per 100

persons and High Cost Loans.

The

Null Hypothesis is that there is no linear relationship between Number of

Foreclosures per 100 persons and Percent of people with Mortgages. The

Alternative Hypothesis is that there is a linear relationship between Number of

Foreclosures per 100 persons and Percent of people with Mortgages.

The

Null Hypothesis is that there is no linear relationship between Number of

Foreclosures per 100 persons and Percent of Black people. The Alternative

Hypothesis is that there is a linear relationship between Number of

Foreclosures per 100 persons and Percent of Black people.

The

Null Hypothesis is that there is no linear relationship between Number of

Foreclosures per 100 persons and Percent of White people. The Alternative

Hypothesis is that there is a linear relationship between Number of

Foreclosures per 100 persons and Percent of White people.

The

Null Hypothesis is that there is no linear relationship between Number of

Foreclosures per 100 persons and Percent of Non-white people. The Alternative

Hypothesis is that there is a linear relationship between Number of Foreclosures

per 100 persons and Percent of Non-white people.

The

Null Hypothesis is that there is no linear relationship between Number of

Foreclosures per 100 persons and Percent of Asian people. The Alternative

Hypothesis is that there is a linear relationship between Number of

Foreclosures per 100 persons and Percent of Asian people.

The

Null Hypothesis is that there is no linear relationship between Number of

Foreclosures per 100 persons and Unemployment. The Alternative Hypothesis is

that there is a linear relationship between Number of Foreclosures per 100

persons and Unemployment.

The

Null Hypothesis is that there is no linear relationship between Number of

Foreclosures per 100 persons and Commuting Minutes. The Alternative Hypothesis

is that there is a linear relationship between Number of Foreclosures per 100

persons and Commuting Minutes.

The

most significant variables were HighCostLoans and PerMortgage10. I know this

because of their low significance values which were close to 0; no other

variables had significance values under the required 0.05. They also had

positive betas which show that they increase as the dependent variable

increase.

At

first there was some multicollinearity because of the variable PerBlack. I knew

this because of the Eigen value that were close to zero and the condition

indexes that were over 30. Once I had removed this variable the

multicollinearity disappeared.

PerNonwhite

was exclude right away meaning that the variable was just so far from

significant the regression didn’t include it. I then removed the remaining

variables that were not found significant which included PerWhite, ComMins10 and

Unemploy10, PerAsian. I had to rerun the statistics five times in order to get

my final equation by removing the least significant variable each time until

there were only significant variables left.

At

first the significance value was 0.090 for PerMortgage10 but by the time that I

had eliminated all other variables beside PerMortgage10 and HighCostLoans the

significance value had gone down to 0.017 which is below the 0.05 needed to be

significant.

For

Number of Foreclosures per 100 persons and High Cost Loans I reject the null

hypothesis. There is a linear relationship between the two.

For

Number of Foreclosures per 100 persons and Percentage of people with mortgages I

reject the null hypothesis. There is a linear relationship between the two.

For

Number of Foreclosures per 100 persons and Percent of Black people I fail to

reject the null hypothesis. There is no linear relationship between the two.

For

Number of Foreclosures per 100 persons and Percent of White people I fail to

reject the null hypothesis. There is no linear relationship between the two.

For

Number of Foreclosures per 100 persons and Percent of Non-white people I fail

to reject the null hypothesis. There is no linear relationship between the two.

For

Number of Foreclosures per 100 persons and Percent of Asian people I fail to

reject the null hypothesis. There is no linear relationship between the two.

For

Number of Foreclosures per 100 persons and Unemployment I fail to reject the

null hypothesis. There is no linear relationship between the two.

For

Number of Foreclosures per 100 persons and Commuting Minutes I fail to reject

the null hypothesis. There is no linear relationship between the two.

My

final equation is y = -0.10 + 0.004x1

+ 0.004x2

The variables

are

y = Number

of Foreclosures per 100 persons (Count2011)

x1

= High Cost Loans (HighCostLoans)

x2

= Percent of people with mortgages (PerMortgage10)

My

results show that high cost loans and percent of people with mortgages have

significant correlations with the number of foreclosures per 100 persons. I can

use this equation to predict the number of foreclosures per 100 persons in a

given census tract if I have the data for high cost loans and percent of people

with mortgages.

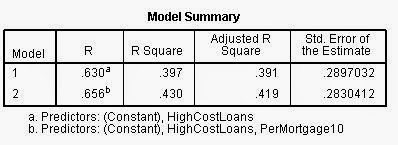

Part III – Stepwise

|

| SPSS results from a Stepwise Regression. |

I ended

up with the same model as the Kitchen Sink Approach:

Final

equation is y = -0.10 + 0.004x1

+ 0.004x2

The variables

are

y = Number

of Foreclosures per 100 persons (Count2011)

x1

= High Cost Loans (HighCostLoans)

x2

= Percent of people with mortgages (PerMortgage10)

The

Stepwise Regression gives me the same model and equation as the Kitchen Sink

Approach, however it does it in one step instead of multiple. That’s awesome

that the stepwise approach can do all of that analysis by itself; it saves time

in having to rerun the regression over and over until I get an equation.

Prediction:

x1

= 80.0 High Cost Loans

x2

= 50.0% Drive to Work

y = -0.10 + 0.004(80.0) + 0.004(50.0)

y = -0.10 + 0.32 + 0.20

y = 0.42

According

to my model, having 80 high cost loans and 50% of people driving to work in a

given census tract you will get 0.42 foreclosures per 100 persons in that

census tract.

I am somewhat

confident in my results due to the okay R2 value of 0.430 that I had

in my model. The high significance that the two variables I used helps the confidence

that I have in the model, but the R2 value is the most important

sign of the strength of a model. So, I would say that my model is moderately adequate.